Which market should a global investor choose? Exact facts, real numbers, costs, risks, and a clear winner at the end were crafted by Dubai Housing, so make the most of it.

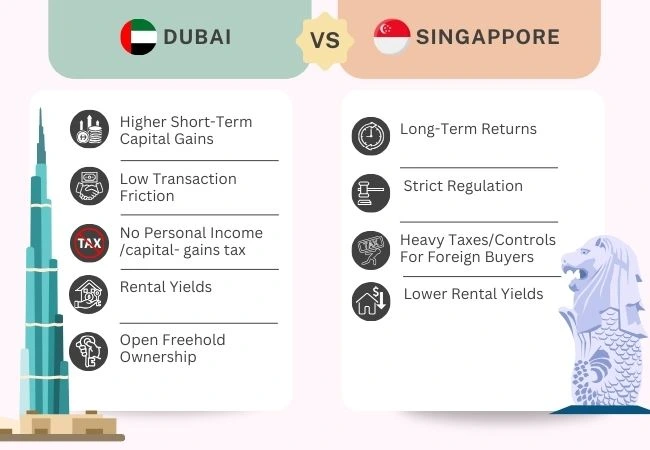

Dubai: Higher short-term capital gains and rental yields, low transaction friction, no personal income/capital-gains tax, and open freehold ownership for foreigners.Strong price growth in 2021–2025 where both apartments and villas have outperformed

Singapore: Stability, predictable long-term returns, strict regulation, and heavy taxes/controls for foreign buyers (very high ABSD), lower rental yields but safer capital preservation in downturns.

Why do people compare Dubai & Singapore?

These are two gateway cities attractive to global capital: Dubai for tax-efficient, high-growth plays and Singapore for safe, regulated, capital-protected holdings. Both appeal to wealthy international buyers, but their rules, returns, and level of risks make them apart.

1) Dubai vs Singapore Market performance (price growth & rents) - latest numbers

Dubai (high growth / high volatility)

Citywide sales prices and rents surged in recent years; citywide residential prices rose strongly in 2021–2024 and continued into 2025 (Residential rents +16% and sales prices +18% YoY in their 2024/25 update). In fact, some prime villa prices have almost doubled in recent years, let us show the data below to understand it better: -

| Time Period |

What Grew (Apartments / Villas / Prime Areas) |

Approx Growth Rate |

| 2020 → 2025 (Central / City-Centre Apartments) |

City-centre / Burj Khalifa / Downtown-type apartments |

122% growth in price per sq. metre in central Dubai from 2020 to mid-2025. |

| 2021 → 2025 (Villas in Prime Districts) |

Villas in places like Palm Jumeirah, Jumeirah Islands, Emirates Hills |

30-40%+ / returns above 4 years for prime villas; in some top zones > +100% in value since 2021. |

| 2021 → 2025 (Luxury / Villa vs Apartment Growth) |

Villas vs Apartments - Villa price index vs Apartment index |

Villas have often outpaced apartments; e.g. villa capital values ≈ 175% above 2021 peaks in some reports. Apartments also rose, but lower in many communities. |

| Year-on-Year change 2024-2025 |

Across all residential property types |

20-30% annual uplift seen in many segments; apartments ~21-25%, villas ~30%+ in several prime areas |

2. Singapore (steady, controlled growth)

Singapore’s private residential price index and rental index show modest, steady increases in 2024 - 2025: URA reported ~1.0% price index increase in Q2 2025 and rental index up 0.8% in Q2 2025 - low, stable growth compared to Dubai’s boom cycles. Public housing resale rose 9.6% in 2024 (HDB), indicating strong domestic demand, but the state maintains tight measures.

| Area / District |

Region (CCR / RCR / OCR) |

Key Indicators of Growth |

Examples & Notes |

| Rest of Central Region (RCR) - e.g. Katong, Geylang, Meyer, Union Square, Eunos |

RCR |

Among the fastest rising in non-landed condos & new launches; median psf growth, high take-ups in launches. |

Projects like Emerald of Katong, Nava Grove, Union Square Residences, The Continuum led strong sales, setting new benchmark psf in RCR |

| Outside Central Region (OCR) - suburbs with new launches, e.g. Sengkang (District 28), Tampines (District 18), Pasir Ris |

OCR |

High % capital appreciation over last several years; latest resale/new launch psf high take up; price power during new project launches |

High Park Residences in District 28 saw ~59% appreciation; OCR still popular for HDB upgraders and affordably priced condos |

| Core Central Region (CCR) - e.g. Marina Bay, Orchard / River Valley, Tanglin, Holland Village |

CCR |

Moderate but improving growth, especially due to luxury / ultra-luxury launches; catching up after cooling measures; premium psf |

CCR showed strong q-o-q rise in some quarters (Q2 2025) especially through new ultra-luxury launches like 21 Anderson, Skywaters Residences |

| District 3 (Queenstown, Alexandra) |

RCR |

High growth in some developments over the past decade; strong demand for well-connected developments |

Examples: Artra (launch to resale psf increase ~42%+), Queens Peak etc |

| District 14 (Geylang, Eunos, Paya Lebar) |

RCR |

Some of the top performing developments in terms of percentage growth over past ~5-10 years |

Named among the top RCR high-growth districts |

| District 18 (Tampines, Pasir Ris) |

OCR |

Strong new launch performance, rising resale prices, demand from families due to amenities/connectivity |

Parktown Residence, Treasure at Tampines etc. |

3) Dubai vs Singapore Taxes & transaction costs - the math that kills or makes deals

Dubai - Low transactional friction, tax-friendly

No personal income tax, no capital gains tax for individuals. Main transaction cost = Dubai Land Department (DLD) transfer fee ~4% plus admin/trustee fees; agent fee ~2% typical. Corporate entities earning rental income may face corporate tax (UAE corporate tax at 9% for profits above the threshold), but individual investors keep rental income largely tax-free

Singapore - Heavy taxation for foreigners

Additional Buyer’s Stamp Duty (ABSD) for foreigners is currently 60% of the purchase price (profile dependent). On top of BSD (tiered up to 6%). Also, Seller’s Stamp Duty (SSD) applies if you sell within specified holding periods, and income tax on rental (progressive for residents; flat 24% for non-residents). These produce very high effective entry costs and can crush short-term returns

See the simpler version of tax and fees through the table: -

| Item |

Dubai |

Singapore |

| Transfer / registration cost |

4% DLD fee + admin (AED ~580 etc.) - one-time. |

BSD (tiered) + ABSD (up to 60% for foreigners) + SSD if sold quickly |

| Annual tax on rental income |

0% personal (individual); corp bodies may pay corporate tax. |

Taxable - residents pay progressive rates; non-residents are taxed on rental income (flat/varies) |

| Capital gains tax on sale |

0% for individuals |

No separate capital gains tax for individuals, but SSD applies to short holdings. |

7) Dubai vs Singapore Property Holding Costs and Maintenance Expenses

Dubai: Lower holding costs (no property tax), but service charges (maintenance & community fees) vary widely across buildings; air-conditioning is a material cost. High short-term rental appetite (tourists, business travellers) also helps

For a better experience, see this: -

| Community / Project |

Typical Service Charge (AED / sq.ft / year) |

| Downtown Dubai - Burj Khalifa |

AED 67.88 |

| Downtown Dubai - The Address BLVD |

AED 65 |

| Downtown Dubai - Vida Residences |

AED 39 |

| Dubai Marina - Range across towers (e.g. Park Island, Princess Tower, Marina Gate) |

AED 12-20 average |

| Dubai Marina - Range across towers (e.g. Park Island, Princess Tower, Marina Gate) |

AED 12-20 average |

| Palm Jumeirah - Apartments & Villas |

AED 10-15 (apartments), Villas similar or slightly higher in luxury ones |

| Jumeirah Lakes Towers (JLT) / Business Bay |

AED 15 (residential) |

| Jumeirah Beach Residence (JBR) |

AED 15.4 |

| Jumeirah Village Circle (JVC) |

AED 9.7-22 |

| Discovery Gardens & International City |

AED 7-12.5 |

| Arabian Ranches (1 and 2) Villages |

AED 3.08 (AR1) / AED 2.44 (AR2) |

| Al Barari Villas / Apartments |

AED 6.9 (villas) / up to AED 17 (apartments in “Seventh Heaven”) |

- Singapore: Higher ongoing taxes and stricter tenancy protections; property management is reliable, but the cost of living and utilities are higher. Short-term leasing is heavily regulated (and sometimes restricted).

9) Two real investor scenarios (worked examples)

A. Yield-focused investor - Dubai example

- Buy a 1-bed apartment in Dubai Marina for AED 1,200,000. Typical gross yield ~6.5% → AED 78,000/yr. No personal tax → net before costs AED 70k. One-time DLD 4% = AED 48,000. Resale potential is high if the market appreciates.

B. Long-term wealth preservation investor - Singapore example

- Buy a 1-bed condo for SGD 1,500,000. ABSD (if foreigner) 60% = SGD 900,000 - massive upfront cost that changes ROI math. Rental yield 3% = SGD 45,000/yr; plus taxes and SSD rules if selling early. You buy stability and safety, not yield

11) Which market “wins”? (Verdict)

Short answer: It depends on your objective.

- If you want higher yields, faster capital gains (and accept more volatility): Dubai is the winner. Tax advantages, high rental yields, and lower entry transaction taxes make it ideal for yield-hungry investors and opportunists. (Winner for yield & growth.)

- If you want stability, wealth preservation, and are ready to pay for regulatory certainty: Singapore wins. It’s a premium, highly regulated market that protects capital and favours long-term, low-risk investors but not for foreigners who want high transactional leverage because ABSD and other measures penalise foreign purchases. (Winner for safety & predictability.)

At the end, let us assume a fixed salary in Dubai and Singapore, so understand the overall cost of living, where the rent, groceries, tax, transport, and more expenses are included to have a complete comparison and better understanding if you want to move place, look at the table below: -

Cost of living- Dubai vs Singapore (Assuming a Salary of US$6,000)

Let’s assume:

- Salary = US$6,000 monthly gross (approx USD equivalent) in both cities (just for comparison)

- Lifestyle: Single person, 1-bedroom apartment, moderate dining, public transport + occasional taxis, basic utilities.

| Expense Category |

Dubai |

Singapore |

| Gross Salary (monthly) |

$6,000 |

$6,000 |

| Income / Tax / Mandatory Deductions |

$6,000 * 0% (Dubai has no personal income tax) = $6,000 take-home. |

After progressive income tax + mandatory contributions, take home ≈ $4,700-$5,000 (depends on exact bracket) |

| Rent (1BR City Centre) |

$1,724 in Dubai center |

$3,000-$5,000 SGD (~US$2,200-3,700) depending on location. We’ll assume $2,800 for a decent place |

| Utilities + Internet + Basic Bills |

$200-300 (electric, water, internet) in Dubai. |

$250-350 (higher utilities, internet, etc.) in Singapore. |

| Food / Groceries / Eating Out |

$400-600 modestly in Dubai. |

$500-700 moderately in Singapore. |

| Transport (public/occasional taxi) |

$100-150 in Dubai |

$200-300 in Singapore. |

| Miscellaneous (entertainment, gym, personal items) |

$200-400 |

$250-400 (likely more in Singapore). |

| Total Monthly Expenses Estimate |

$2,800 - $3,500 (depending on lifestyle) |

$4,000 - $4,700 |

| Result: Monthly Leftover (Savings / Discretionary) |

$2,500 - $3,200 |

$700 - $1,300 |

So you can clearly this the difference in both the places where only the investment is not just a concern, but also the cost of living makes an overall impact, so think wisely before investing in any of these reputed areas in the world that hold potential and growth.

Overall winner for most international investors (2025):

- For active investors seeking returns and tax efficiency → Dubai.

- For ultra-risk-averse capital preservation and residency/family reasons → Singapore.

.webp&w=828&q=75)